Are Things Getting Stretched?

Is Extreme AI-Driven Profitability Plausible?

An article in today’s news scan really caught my eye

S&P 500 Q1 2026 Earnings: +29% YoY EPS Growth — Strongest in Four-Plus Years, More Than Double Pre-Season Forecasts

Source: Charles Schwab market analysis

Date/Time: June 2, 2026 (season summary)

The first-quarter 2026 earnings season closed with S&P 500 companies reporting approximately 29% annual earnings-per-share growth — the strongest result since late 2021 and more than double the ~13% consensus forecast on March 31. The beat is largely AI-driven: hyperscaler revenue recognized on massive infrastructure deployments, semiconductor pricing power (South Korea May exports confirmed $37B+ semiconductor revenues), and AI-enabled efficiency gains across enterprise software margins. Corporate America is absorbing the war-era energy cost shock with minimal margin compression. The significance for the macro picture is as a counterweight to the stagflation narrative: if corporate earnings are running at 29% even as inflation accelerates, the real economy is absorbing the cost shock far better than headline stagflation framings suggest. This creates a specific policy challenge — standard monetary tightening theory assumes profit margins compress when rates rise, cooling demand. But if AI productivity gains are sustaining 29% profit growth through a war-era energy shock, central banks may need to tighten substantially more than simple inflation-targeting models imply to actually cool aggregate demand. The earnings data are a structural validation of the “higher for longer” and potentially “higher than expected” rate thesis — not just for the Fed, but globally.

Schwab

Something I’ve written about a fair amount is that the only thing supporting the US consumer is the wealth effect from their equities continuing to go up, and the only thing that’s keeping equities going up is a few AI companies.

My former colleague Bob Elliott took a look at the expectations baked into the equity market with an eye on this same question; he looks at what it would take for this process that supports the consumer to continue. And what he finds isn’t pretty.

He starts by stating what is priced in.

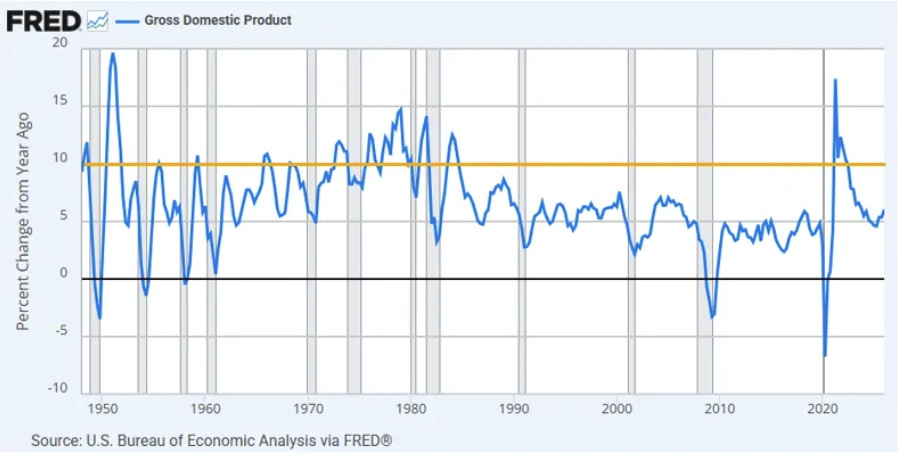

The first quarter’s notably strong 28% earnings growth is not being seen as a one off event, but instead increasingly expected far out into the future. Analysts are now expecting an additional 20% growth over the next year and 22% on average over the next 5 years, the highest in recorded history absent the surge out of the covid stop.

While there have been several individual quarters of earnings growth this strong in history, the math behind a prolonged period of very high earnings growth becomes increasingly tenuous. Ultimately earnings growth can come from either increasing sales or increasing margins. If you take the 22% number at face value, it barely makes it with 10% nominal sales growth and 2% margin expansion *per year* over the next 5 years.

The AI story certainly promises that things like this are possible, and the market pricing is showing that people think it’s plausible. But something I’ve learned in my career in macro investing is that everything is connected — market pricing is just cash flows and discount rates which is just growth and inflation (and liquidity and risk premiums) and a change in one thing causes a change in all the other things which then causes a change in more things which eventually changes the first thing. You have to get the sequence right to get what is likely to transpire right, which you can then compare to what is priced to transpire to hopefully make some money.

So the next thing Bob looks at is the set of economic conditions that would have to transpire to make the market pricing come true over time.

But it’s not just a math problem, these inputs have to be reconciled with real economic outcomes. Sales figures for instance rarely diverge from nominal GDP growth over meaningful periods of time. S&P 500 sales growth over the last 10 years and US nominal GDP growth have both been 5-6%. So hitting 10% nominal sales growth likely requires a similar rate of nominal GDP growth for 5 years, an outcome only seen during the inflationary 70s.

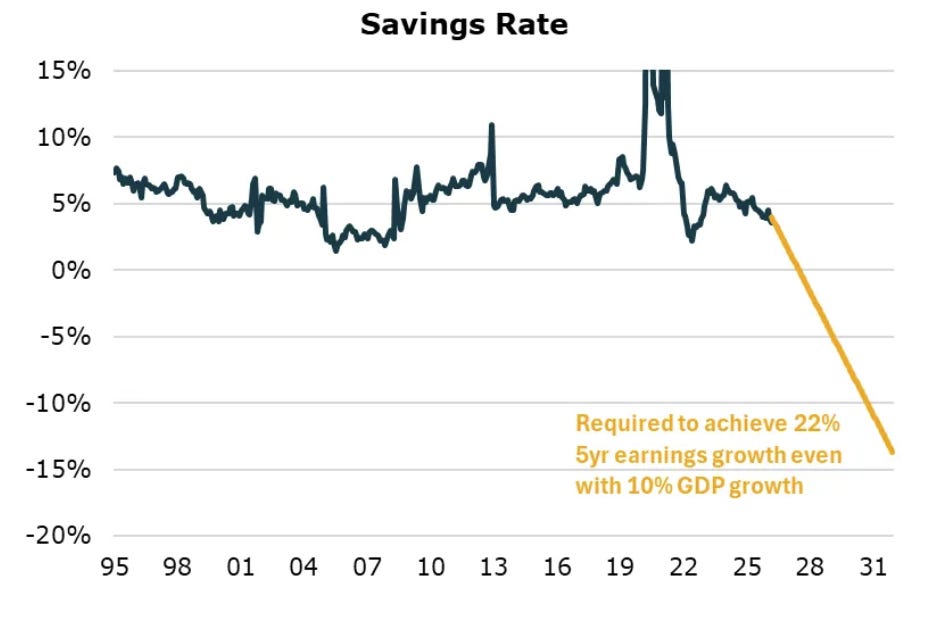

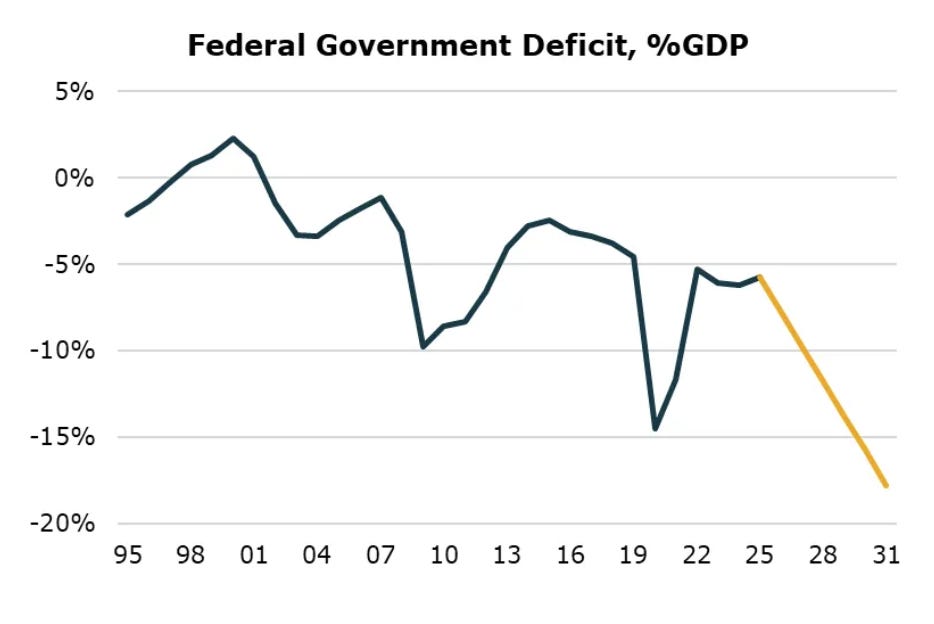

It also requires extreme margin expansion, rising from 15% today to 25% a mere 5 years from now, which also has to be reconciled with real world outcomes. The only way for the corporate sector to increase their margins (essentially increasing their savings rate) is that another sector reduces their savings to a similar degree (essentially reducing their savings rate). For those less familiar with the accounting mechanics, check out the Kalecki framework.

Getting a 10% rise in corporate margins through labor cost reduction requires labor to cut their savings by 10% of GDP (or about 15% of disposable income). Or if it is offset by government deficits, a 10% increase in the Federal government deficit. Such outcomes would be extraordinary in any historical context to the point of being implausible.

He then has a bunch of great charts to illustrate the points. Like this one of how the 10% nominal growth that’s priced to happen each year for the next five years compares to how it’s come in historically.

Or what the priced-in margin expansion would look like.

Or, on a topic that I’ve been particularly interested in, what it would take from the household and government sectors if the way these growth and margin targets are hit is that AI makes companies vastly more profitable by making labor obsolete.

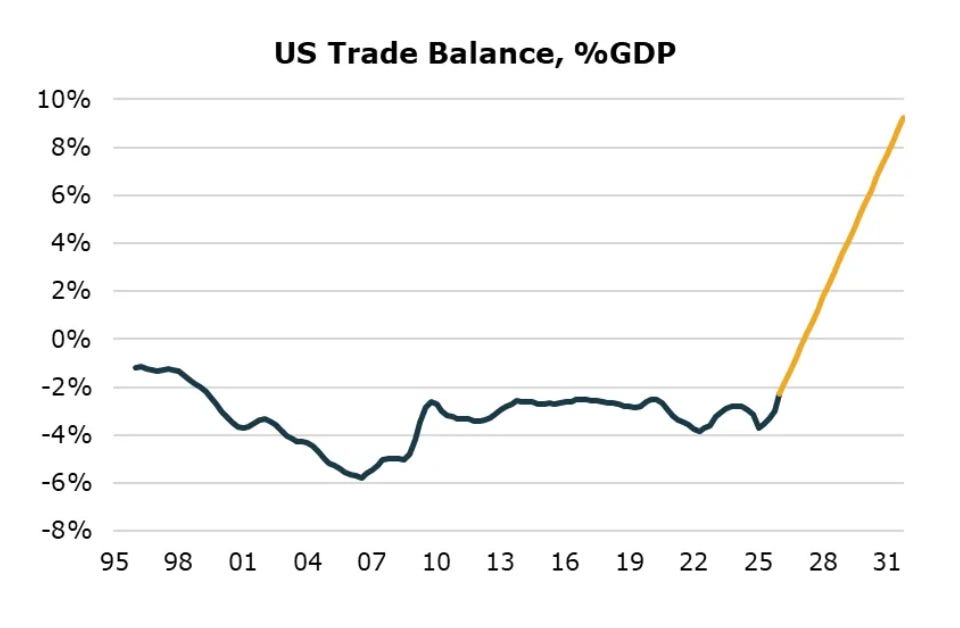

He even hits the possibility that AI makes US companies so globally competitive that these profits are funded by the rest of the world.

The takeaway from all of this is that the stock market is pricing AI to be a truly transformative technology, but for this transformation to actually take place, two things must be true:

The balance of income between the corporate, household, and government sectors needs to radically shift to extreme levels that are almost literally off the charts

This radical shift does not collapse society, which would collapse the stock market

The problem with this analysis is that, like I said earlier, getting the order of how things go matters a lot. You can see how things will play out, but if you bet on step 5 while ignoring the sequencing of steps 1-4, you’re going to lose your shirt. So I agree with Bob that things seem stretched, but who can say how much longer things have to run?

News Scan

Iran Formally Suspends US Ceasefire Talks Over Lebanon Scope Dispute; Brent Surges 5% to ~$95; Israel-Lebanon Extend 45-Day Ceasefire

Source: Bloomberg, Reuters, Washington Post, CNN

Date/Time: June 1–2, 2026

Iran’s negotiating team halted all communications with Washington via mediators on June 1, citing Israel’s expanding military offensive in southern Lebanon as a violation of the ceasefire. The core dispute is definitional: Tehran insists the US-Iran ceasefire constitutes “a comprehensive ceasefire across all fronts, including Lebanon,” while US officials — including Trump and Vance — maintain Lebanon was never part of the deal. Netanyahu separately said Israeli strikes would continue “as planned.” CENTCOM reported intercepting Iranian-launched missiles aimed at Kuwait. Brent crude jumped roughly 5% intraday to ~$95/barrel, partially retracing the ~20% decline from April peaks that had built on ceasefire optimism; the intraday reversal came after Trump contradictorily claimed talks were “continuing at a rapid pace” and that a Hormuz MOU could be reached “within a week.” On a parallel track, Israel and Lebanon agreed to a 45-day extension of their bilateral ceasefire — a de-escalation signal on one front that has no immediate bearing on the Iran-US nuclear talks. June 2: Trump is actively lobbying Israel to ease its Lebanon posture to preserve the Iran talks. The formal suspension marks a qualitative escalation from the “stalled” characterization as of the prior scan; the Lebanon inclusion dispute creates a structural impasse that neither side can easily concede. Iran cannot be seen to accept a ceasefire that leaves Hezbollah exposed; the US cannot pressure Israel into a Lebanon withdrawal without risking the collapse of its regional coalition. Oil at $95 reflects markets repricing the probability that the 60-day MOU will not be signed before the June window closes.

Washington Post

EZ HICP Flash May: 3.2% (First Above 3% Since 2023), Core 2.5%, Services 3.5% — ECB June 11 Hike Fully Priced

Source: Bloomberg, Eurostat, ActionForex

Date/Time: June 2, 2026

Eurozone flash CPI for May printed 3.2% YoY — above 3% for the first time since approximately mid-2023 and beating consensus of ~3.0%. Core CPI accelerated from 2.2% in April to 2.5% (above the 2.4% estimate). The most notable move was in services, which surged from 3.0% to 3.5% — a 50bp jump in a single month that signals demand-side inflation is now spreading beyond the initial energy shock. Energy remained the largest contributor at 10.9% YoY. The data closes the loop on ECB pricing: the June 11 rate hike (+25bp, DFR → 2.25%) is now effectively priced at 100%, validated by three weeks of executive board messaging (Schnabel, Pereira, Villeroy) plus today’s hard data confirmation. A September hike is running at ~50%.

The read-across to the US is direct: with European services inflation now demonstrably spreading through the domestic economy — not just the energy component — the global “supply shock fades on its own” thesis is being revised upward for duration and magnitude. The 3.5% services reading in particular provides ammunition for every hawkish CB globally, since services inflation is wages, rent, and domestic demand — not oil. It is far more persistent and far harder to look through than a commodity spike.

ActionForex

Markets Price 60% Odds of Fed December Rate Hike; 10-Year Treasury Yield Rises 6bps to 4.51%

Source: Rio Times Online / Global Economy Briefing, CME FedWatch

Date/Time: June 2, 2026

Fed Funds futures as of Tuesday priced approximately 60% odds of at least one rate hike by December 2026 — the first time in this cycle that outright tightening is the modal scenario rather than a minority tail. The 10-year Treasury yield rose 6 basis points to 4.51%, reflecting higher near-term inflation expectations (EZ CPI beat, Iran ceasefire suspension repricing energy) and a shifting rate path. The December pricing matters because it precedes Warsh’s inaugural FOMC press conference on June 17, where the dot plot and new chair’s language will clarify whether the Fed’s reaction function has formally pivoted toward tightening. The June meeting itself is expected to hold at 3.50–3.75%, so the action is entirely in the forward signal. The Fed’s path is being repriced not because of a US-specific shock but because of a convergence: EZ CPI confirming services inflation is demand-embedded, oil retesting highs on Iran talks suspension, and US manufacturing and services data remaining firm. If December hike odds move above 70%, the housing market — already under pressure from the Iran war cost pass-through — faces an additional rate shock, since mortgage rates benchmark to 10-year yields now at 4.51%. The Fed premium applies here: even a market-implied signal about Fed rate direction is more actionable than most explicit signals from other central banks.

Global Economy Briefing

Alphabet Raises $80 Billion for AI Infrastructure: $30B Public Offering + $40B ATM + $10B Berkshire Hathaway

Source: Bloomberg, SEC filing, GuruFocus

Date/Time: June 1, 2026

Alphabet announced the largest equity capital raise in tech history: a $30 billion concurrent public offering ($15B in mandatory convertible preferred stock and $15B in Class A/C common stock), a $40 billion at-the-market program launching Q3 2026, and a $10 billion private placement with Berkshire Hathaway ($5B Class A at $351.81/share; $5B Class C at $348.20/share). The Berkshire private placement is the most structurally significant element: Buffett’s firm has historically avoided tech equity at scale, making this an unambiguous institutional endorsement of AI as a real-economy investment story — not a speculative cycle. Stock fell 2–3% on dilution anxiety, a notable response: $80B is larger than any prior capital raise in the sector, and the market’s muted-to-negative reaction signals that equity issuance capacity for AI is being stress-tested even as the capex thesis remains intact. Total 2026 capex for the top five hyperscalers now sits at a consensus $720 billion. SpaceX, OpenAI, and Anthropic are in various stages of capital raising that could add another $200B+ in AI equity demand. Alphabet’s pricing ($351.81 for Class A) sets the benchmark for the queue behind it. For capital markets, the absorption question is real: can markets continue to fund $700B+ in annual AI capex at current equity multiples while simultaneously repricing the risk-free rate upward? That tension defines the 2026 macro regime.

Bloomberg

Nvidia RTX Spark Superchip Enters Consumer PC Market at Computex 2026; NVDA +6.3% (+$319B)

Source: CNBC, Bloomberg, Tom’s Hardware

Date/Time: June 1, 2026

Nvidia CEO Jensen Huang unveiled the RTX Spark superchip at Computex in Taipei — an ARM-based SoC integrating a Blackwell GPU (6,144 CUDA cores), 20 CPU cores, and 128GB of LPDDR5X unified memory, targeting Windows laptops from Dell, HP, Microsoft (Surface), Asus, Lenovo, and MSI. Fall 2026 availability. Performance positioned as equivalent to the RTX 5070 laptop GPU. Nvidia shares rose 6.3%, adding approximately $319 billion in market cap in a single session — among the largest single-day market cap gains in corporate history. The move shows the AI investment thesis remains intact at the consumer hardware level even as the global macro picture clouds. The macro read is structural: AI is transitioning from an infrastructure-buildout phase concentrated in hyperscaler data centers to a consumer hardware adoption cycle. This broadens the addressable market significantly while also pulling AI monetization timelines forward. Goolsbee’s May 28 framing — that anticipated AI productivity gains pulling forward current investment are themselves inflationary — becomes more urgent if the consumer phase accelerates demand. For central banks already hiking on war-driven energy inflation, the additional demand impulse from an AI hardware consumer cycle is another reason rates need to stay higher longer.

CNBC

US Tariff Reduction: Farm and Construction Equipment Drops to 15% from 25%, Effective June 8

Source: Bloomberg, White House fact sheet

Date/Time: June 1–2, 2026

Trump signed an executive order reducing tariffs on farm and construction equipment — combines, harvesters, forklifts — from 25% to 15%, effective June 8 through December 31, 2027. Foreign manufacturers qualify for a further reduced 10% rate if the equipment contains at least 85% US-origin steel or aluminum. The explicit rationale is war-era cost relief: US farmers have absorbed surging input costs from Iranian conflict-driven energy inflation, and the administration is deploying targeted tariff relief as an alternative to broader fiscal intervention. This is one of the first explicit examples of trade policy being used as a demand-side inflation management tool in the current war context. The direct fiscal cost is modest (narrow product categories), but the precedent is notable — it signals the administration is willing to use tariff reductions selectively to offset war-related input cost shocks rather than allowing demand destruction to do the inflation-correction work. If the model is extended to other categories — fuel, fertilizer, broader agricultural inputs — it represents a structural shift in how Washington manages the inflation-growth tradeoff under geopolitical stress.

Bloomberg

UK Mortgage Approvals: 65,945 in April (15-Month High); BOE Data

Source: Bank of England (via Bloomberg, MarketScreener)

Date/Time: June 2, 2026

Bank of England data released June 2 showed 65,945 mortgage approvals in April — up from 63,979 in March and the highest since January 2025. The reading surprised to the upside relative to analyst forecasts. Net mortgage lending fell to £4.37 billion (lowest since October 2025), reflecting a bifurcated market: approval volume is resilient but actual net credit extension is declining as buyers size down or existing holders pay off more. The BOE’s current base rate is 3.75% (held since December 2025), with the next decision June 18 where a hold is the expected outcome.

The housing resilience matters in the context of BOE governor Bailey’s “second-round effects” gating variable: if demand in rate-sensitive sectors like housing remains robust at 3.75%, the criterion for tolerating above-2% inflation becomes harder to sustain. The second-round risk is present precisely because demand hasn’t broken. Combined with Ofgem’s confirmed 13% energy cap increase effective July 1, the UK faces a summer where both energy-push and demand-pull inflation channels are active simultaneously — a difficult position for a BOE that has been the most dovish among G7 central banks this cycle.

MarketScreener

Japan Jibun Bank Services PMI May Final: 50.0 (From 51.0); BOJ June Hike Headwinds Accumulate

Source: S&P Global / Jibun Bank, FXStreet

Date/Time: June 2, 2026 (final reading)

Japan’s Jibun Bank Services PMI final reading for May came in at 50.0 — the precise borderline between expansion and contraction — down from 51.0 in April. Manufacturing held firmer at 54.5 (from 55.1) but was also cooling. The services deceleration matters directly for BOJ: the bank’s upcoming rate decision is conditional on evidence that the wage-price spiral is self-sustaining through the domestic services sector. A services PMI at exactly 50.0 is insufficient confirmation of that dynamic. This compounds a deteriorating picture for the June hike thesis: the prior scan confirmed Japan Q1 capex came in at +0.047% YoY versus a 4.0% forecast (manufacturers citing Iran war uncertainty for postponing capital investment), and Tokyo CPI for May decelerated for the sixth consecutive month to 1.3%, below BOJ’s 2% target. BOJ is caught between a 6-3 April split vote that signaled hawkish intent and incoming data that is sequentially softening the case for immediate action. Three separate legs of the “virtuous cycle” argument — capex, services activity, consumer prices — are all weakening simultaneously. The June hike remains possible given the dissents, but requires BOJ to override the data rather than be guided by it.

FXStreet

ECB’s Schnabel at Bank of Korea Conference: Stablecoins Threaten Monetary Policy Transmission and Financial Stability

Source: ECB (via EuropeSays)

Date/Time: June 2, 2026

ECB Executive Board member Isabel Schnabel spoke at the Bank of Korea International Conference on “Central Banks and the Future of Money,” delivering a direct warning that stablecoin proliferation — particularly dollar-backed stablecoins — poses structural risks to monetary policy transmission and financial stability. Schnabel argued that central banks must “keep pace with innovation to preserve the anchoring role of central bank money in the future monetary system.” This adds an ECB institutional dimension to the stablecoin policy debate opened by Fed Governor Waller on June 1, who framed dollar stablecoins as an amplifier of US monetary policy reach. The two speeches arrive at the same phenomenon from opposite directions: Waller sees dollar stablecoins extending the Fed’s influence globally; Schnabel sees them as a bypass mechanism that weakens non-US central banks’ ability to control domestic monetary conditions. For the ECB specifically, the concern is direct — widespread adoption of dollar-backed stablecoins in European retail payments would effectively import Fed rate decisions into the eurozone independent of ECB policy. For global macro, the ECB-Fed framing divergence illustrates the geopolitical fault line in digital money: US-issued stablecoins are simultaneously a tool of dollar hegemony and a structural risk to every other central bank’s monetary sovereignty.

EuropeSays

S&P 500 Q1 2026 Earnings: +29% YoY EPS Growth — Strongest in Four-Plus Years, More Than Double Pre-Season Forecasts

Source: Charles Schwab market analysis

Date/Time: June 2, 2026 (season summary)

The first-quarter 2026 earnings season closed with S&P 500 companies reporting approximately 29% annual earnings-per-share growth — the strongest result since late 2021 and more than double the ~13% consensus forecast on March 31. The beat is largely AI-driven: hyperscaler revenue recognized on massive infrastructure deployments, semiconductor pricing power (South Korea May exports confirmed $37B+ semiconductor revenues), and AI-enabled efficiency gains across enterprise software margins. Corporate America is absorbing the war-era energy cost shock with minimal margin compression. The significance for the macro picture is as a counterweight to the stagflation narrative: if corporate earnings are running at 29% even as inflation accelerates, the real economy is absorbing the cost shock far better than headline stagflation framings suggest. This creates a specific policy challenge — standard monetary tightening theory assumes profit margins compress when rates rise, cooling demand. But if AI productivity gains are sustaining 29% profit growth through a war-era energy shock, central banks may need to tighten substantially more than simple inflation-targeting models imply to actually cool aggregate demand. The earnings data are a structural validation of the “higher for longer” and potentially “higher than expected” rate thesis — not just for the Fed, but globally.

Schwab

Disclaimer: The information provided on this blog is for informational purposes only and should not be considered investment, financial, or other professional advice. Nothing on this site constitutes a recommendation or solicitation to buy or sell any securities. You should consult with a qualified financial advisor before making any investment decisions. Investing involves risks, including loss of principal.