I’ve written before about Bloomberg Opinion columnist Allison Schrager’s bad opinions, but sometimes it’s good to have a foil you can draw upon for inspiration.

She’s back at it again, with a column on an important topic but with milquetoast (and wrong) takes.

Thanks for reading All In The Reflexes! Subscribe for free to receive new posts and support my work.

She starts by identifying a real problem.

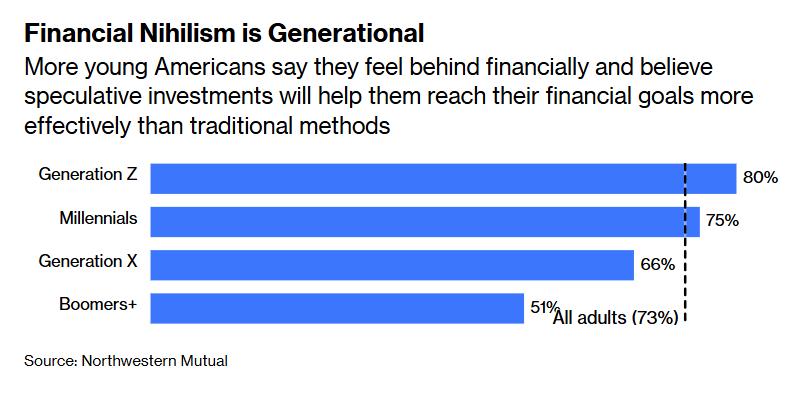

A recent survey from Northwestern Mutual shows that many young people are betting on unconventional high-risk assets because they believe it is the only way to build wealth. It also reveals some good news: Despite a year marked by wild market swings and deep economic uncertainty, more people feel financially secure than they did a year ago, including 39% of Gen Zers (up from 36%) and 52% of millennials (up from 43%). Just a few years ago meme stocks were all the rage, but now it is just straight up gambling, excuse me prediction markets. Some 32% of Gen Zers say they gamble in crypto or sports betting; 35% of millennials own crypto, while 24% bet on sports. Less than 20% of either invest in options or meme stocks. Even more surprising, many of those who don’t feel financially secure believe the only way to reach their goals is to take big risks.

More young Americans say they feel behind financially and believe speculative investments will help them reach their financial goals more effectively than traditional methods

It is a core truth of financial markets that higher rewards come with more risk. But some risks are better than others. Betting big on March Madness may mean bigger potential payoffs than investing in the S&P. But the stock market is much more likely to help people build wealth over time.

But then diagnoses it with some Boomer folk wisdom.

But even if things are hard, they are not harder than they used to be. It is normal for people in their 20s to feel like the economy is stacked against them. It is a hard time of life, economically if not socially, but there is not much evidence that it is worse than before. The median household under 30 in 2022 had higher wages and wealth than the same group did in 1989. There is also a lower risk of losing your job, and while unemployment for young people has been higher lately, it is still lower than many non-recessionary periods of the past.

Another answer to the question of why may be lack of financial education. Most people don’t know how to invest, and people pushing high-risk, high-reward strategies are all over social media. Even financial professionals get swept up in the hype of a bull market — and most investors under 30 have only ever experienced a bull market. (The stock market did fall in 2020, but it came back fast and harder than ever.) A risky market tends to push up the performance of other risky, high-beta assets. Finally, there is evidence that if people are less experienced at risk-taking, which many younger people are, they may be more prone to taking risks with bigger downsides.

If these kids and their avocado toast would just read a book (or a Bloomberg Opinion column), they’d be able to buy a house for three nickels just like me and get a job as an MD at a bank with just a handshake and previous work experience selling nitrous balloons in the parking lot of a Dead concert.

Kyla Scanlon addresses the same topic, and does a much better job pulling all the threads together — it will be nothing new if you are a regular reader here.

I think she misses the mark with her diagnosis as well; she thinks it’s due to a loss in trust in society because the Trump administration is so untrustworthy. I believe that many Democrats honestly think this is the reason they feel this way, so I’m not going to tell anyone their feelings are wrong, but this sort of fall into degeneracy was happening before Trump was President, so I can’t see it as being the root cause.

Also, a very scary health situation she’s going through. Unironically, there are some Bulgarian bodybuilders on Twitter who could probably solve this. A good resource to start with is here.

John Arnold, formerly of Enron and now a philanthropist, gets closer to the mark, pointing to a New York Times article on the subject.

I’ve previously written about how AI will accelerate this trend, but the thing that should scare you (if you’re not a Boomer) is that this was already happening, even before AI came along.

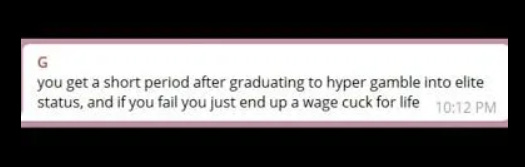

The best treatment on the topic I’ve seen comes from a crypto degenerate a year ago (best to ignore the commentators and listen to the man in the arena).

long degeneracy is your college friend sports betting. long degeneracy is your uncle trading options. long degeneracy is your participation in an online community instead of an irl one. these trends are modern efficiency applied to human nature - the shortest-term reward cycles.

forces like ai only accelerate long degeneracy - at its core there is an understanding that the time to “make it” is running out, and any new developments only shorten the clock.

and though one might be tempted to try and save the world with this knowledge, it is a very large ship headed for the rocks. it is far more practical to ensure you have a safe spot on a lifeboat than it is to turn the ship around.

The key reason people go long degeneracy is the cost of housing.

the core issue here is the cost of owning a house, and the expected timeline on an average salary. with this core social contract broken, people look for shortcuts. crypto, memestocks, and the rise of option and leverage trading are examples of the public’s increasing desire for volatility and asymmetric upside when linear can’t buy a house.

Importantly, the type of inequality that is the problem here is wealth inequality, not income inequality; when inequality is discussed it is usually the income variety, and the solutions to that will not necessarily move the needle on this.

the key underlying factor is growing income to asset inequality. not the ratio of highest earners to lowest earners, but the relationship between wages and the cost of a house.

as this continues to worsen, it will only make the linear timeline - get a normal job, save up for a house - longer and longer, until it becomes completely untenable. this is an example of an expected return (“get a good job after college”) compressing, and this fundamentally drives the search for higher yield in the form of riskier investments.

Contra Kyla Scanlon from above, it was not the Trump administration that did this, but rather QE. QE 1 was probably necessary, but every subsequent round of quantitative easing pulled asset returns from the future to the present (which, for a thing that already happened, is our past — nobody told you there would be time travel in today’s article), boosting the wealth of the people who held assets at that time by transferring it from people who might want to hold those assets in the future.

Someone else who sees QE this way is new Federal Reserve Chair Kevin Warsh.

I doubt Warsh would prescribe long degeneracy as the way out of the situation, and if anything I think it’s more likely that he crashes everything to give a clean slate. I’m also skeptical that any sort of redistributive policies could get us out of the harmful, degenerate spiral. As the Man in the Arena from the long degeneracy post says:

it is the author’s belief that if Unversal Basic Income is ever implemented, it will accelerate long degeneracy to new levels. live life as a stipend peon, or swing for elite status. after all, if you can simply try again next month, what’s the downside of speculating with this month’s check?

So we really are in a pickle. Right now the financial nihilism that this pickle is generating is being channeled into degeneracy, but a degeneracy that our social system condones. The longer things go on this way, though, the more likely it is that this degeneracy escapes the containment area of Polymarket and DraftKings and turns into something more impactful.

News Scan

Houthis Open New Front: Missile Barrage Hits Israel, Red Sea Closure Threatened

Source: Bloomberg / Al Jazeera / Time Date/Time: March 28–29, 2026 Yemen’s Houthi movement fired a barrage of ballistic missiles at southern Israeli targets on March 28–29, explicitly joining the Iran war and opening a new geographic front. The Houthis declared attacks would continue “until the aggression against all fronts of the resistance ceases,” naming Iran and Hezbollah as the other fronts they’re defending. Critically, the Houthis also warned they could close the Bab el-Mandeb strait at the southern entrance to the Red Sea — which, if acted on, would compound the Hormuz closure to threaten both major oil export corridors simultaneously. Hormuz alone disrupts roughly 20% of global oil supply; adding Bab el-Mandeb would extend the supply shock to flows from the Persian Gulf to Europe via the Suez Canal. Markets are now pricing both straits as potential chokepoints. Time

Iran Rejects Pakistan Diplomacy; War Enters Fifth Week With No Breakthrough

Source: Reuters / Fortune / CNN / Al Jazeera Date/Time: March 29–30, 2026 Despite a multilateral diplomatic push in Islamabad — involving Egypt’s Badr Abdelatty, Turkey’s Hakan Fidan, and Saudi Arabia’s Prince Faisal — Iran’s parliament speaker dismissed the talks as “cover” for continued US troop deployment to the region, and Tehran reiterated conditions for negotiations that include a halt to US-Israel strikes. As a limited goodwill gesture, Iran conditionally allowed 20 Pakistani-flagged vessels to transit Hormuz — the first easing of passage restrictions since the closure began — though commercial traffic overall remains near zero. The divergence between Iran selectively unlocking Hormuz for diplomatic partners versus its public rejection of US talks suggests it is using the strait as a targeted coercive tool. Oil executives have warned the strait must reopen structurally by mid-April or supply disruptions become significantly worse. Fortune

BOJ March Meeting Summary Reveals Hawkish Shift: Members Debate Size of Next Hike

Source: Bloomberg Date/Time: March 30, 2026 The Bank of Japan released its Summary of Opinions from the March 19 meeting — the first detailed look at internal deliberations after the 8-1 vote to hold at 0.75%. The summary shows a meaningfully more hawkish internal picture than the decision implied: one board member stated the BOJ “will need to raise the policy interest rate without hesitation” if small-firm wage conditions hold, and internal debate has shifted from whether to hike to how much. At least one member explicitly flagged the possibility of a 50bp response to the oil shock’s inflationary pressure rather than the standard 25bp. The one dissenter, Hajime Takata, voted for an immediate hike to 1%. Markets are now pricing a significantly higher probability of an April hike. The BOJ’s narrative has quietly shifted from “patient normalization” to “acting without hesitation.” Bloomberg

Yen Crosses 160; Japan FX Chief Delivers Final Warning; S&P Flags Downgrade Risk

Source: Bloomberg / Japan Times / ActionForex Date/Time: March 30, 2026 The yen crossed 160 versus the dollar — the level that triggered direct Bank of Japan intervention in 2024 — and Japan’s Vice Finance Minister Atsushi Mimura delivered his strongest threat yet: “If this situation continues, we believe decisive action may soon be necessary.” BOJ Governor Ueda reinforced the signal, saying currency movements have “a big impact” on the economy and on prices. S&P Global Ratings simultaneously warned it could lower Japan’s A+ sovereign rating if the yen weakens “much further,” citing deteriorating economic competitiveness and widening fiscal deficits. The convergence is notable: the BOJ’s hawkish summary is in direct tension with yen weakness driven by the dollar’s safe-haven bid from the Iran war. A forced BOJ intervention or early rate hike could trigger rapid yen appreciation and significant JGB repricing. Bloomberg

Source: Bloomberg / CNBC / Polymarket Date/Time: March 30, 2026 The first post-war read on eurozone consumer inflation expectations showed a sharp upward jump, with financial markets now pricing euro area inflation near 4% over the next 12 months — roughly double the ECB’s pre-war projections. Prediction market Polymarket shows the probability of an ECB rate hike in 2026 has risen to 42%, up from 12% before the Iran conflict began. This matters directly for ECB policy: Lagarde said on March 25 that she is ready to hike rates even if the inflation surge proves “not-too-persistent” — making the consumer expectations data a gating variable for her reaction function. The ECB’s adverse scenario already projects a 4% inflation peak; the most severe scenario exceeds 6% by early 2027. Consumer expectations drifting above 4% would significantly increase pressure on Lagarde to move. Bloomberg

Germany March Flash CPI Points to Highest Inflation in Over a Year

Source: Bloomberg Date/Time: March 30, 2026 German state-level CPI data released March 30 points to Germany’s national flash CPI hitting its highest level in more than 14 months, driven almost entirely by energy costs from the Iran war. Germany had seen inflation fall to 1.9% in February — its lowest in years — before the war reversed the trend sharply. A strong March print validates the ECB’s adverse-scenario inflation forecasts and compresses the timeline before a potential rate hike becomes necessary. The Eurostat euro area flash estimate for March is due March 31 and is expected to show a similar energy-driven spike. Together, Germany and the broader euro area CPI data will be among the most closely watched data points for the ECB’s April decision calculus. Bloomberg

UK Mortgage Rates Cross 5% for First Time Since Late 2024; Lenders Reprice en Masse

Source: MoneySavingExpert / HomeOwners Alliance / BOE Date/Time: March 30, 2026 UK mortgage rates have crossed 5% for the first time since late 2024, with Barclays and Nationwide pulling their sub-4% products and repricing upward across their entire fixed-rate ranges. The Bank of England held Bank Rate at 3.75% at its March 18 meeting, but private market rates are now tightening independently of the policy rate — a sign that lenders are pricing in either future BOE hikes or higher risk premia from the oil shock. UK CPI remained at 3.0% in February, already above the BOE’s target before energy costs from the Iran war fully pass through. The mortgage market repricing represents a de facto tightening of credit conditions beyond what the MPC has formally decided, and could dampen housing activity and consumer spending ahead of the BOE’s April 30 decision. HomeOwners Alliance

JPMorgan, Pimco Warn Bond Market Is Mispricing the Slowdown Risk

Source: Bloomberg Date/Time: March 29, 2026 Some of the world’s largest fixed income managers — including Pimco ($2T+ AUM) and JPMorgan — are publicly breaking with the consensus view that the Iran oil shock is primarily an inflation story. Their argument: history shows inflation shocks of this magnitude “tend to migrate into growth shocks,” and the bond market is currently underpricing that transition. Goldman Sachs puts the probability of a US recession in the next 12 months at ~30%; Pimco puts it above one-third. Pimco CIO Daniel Ivascyn said his firm is positioning for a bond-market rebound driven by eventual yield declines, not the hike cycle the market is now pricing. The practical implication is a divergence between the rates market (pricing hikes from the Fed and ECB) and the real-economy view (pricing a slowdown that ultimately forces cuts). These two views cannot both be right, and the resolution will be the dominant macro trade of Q2. Bloomberg

Brent Crude Heading for Largest Single-Month Price Jump in History

Source: Reuters / Bloomberg Date/Time: March 29–30, 2026 With Brent crude trading in the $115–116/barrel range as the month closes, Brent is on track for the largest single-month price increase in the recorded history of the oil market — surpassing the 2022 Russia-invasion spike. The price has risen from around $75/barrel before the Iran war began in late February, an increase of roughly 55% in under five weeks. Oil executives have issued a coordinated warning that the Strait of Hormuz must reopen structurally by mid-April or supply conditions become significantly worse as emergency stocks are drawn down. The record monthly move matters as a calibration benchmark: none of the standard energy shock scenarios used by the Fed, ECB, or BOJ were designed for a shock of this speed and magnitude. Reuters

Supply Workarounds Emerge: US Approves Russian Oil to Cuba; China Sends Diesel to Southeast Asia

Source: Bloomberg Date/Time: March 29–30, 2026 Two parallel supply relief developments have emerged as downstream responses to the Hormuz closure. The US authorized a Russian oil tanker carrying approximately 100,000 tons of oil to dock in Cuba, addressing energy shortages in the Caribbean traced back to the Middle East supply disruption. Separately, Chinese cargoes of diesel and fuel appeared in Southeast Asia over the weekend despite earlier Chinese export restrictions — suggesting Beijing is quietly releasing strategic reserves to stabilize regional markets. These workarounds are partial and insufficient to replace the volume normally transiting Hormuz (roughly 20% of global daily supply), but they signal that major powers are beginning to use alternative supply channels to manage the economic fallout. The US approval of a Russian tanker represents a notable carve-out from the broader sanctions architecture. Bloomberg

Disclaimer: The information provided on this blog is for informational purposes only and should not be considered investment, financial, or other professional advice. Nothing on this site constitutes a recommendation or solicitation to buy or sell any securities. You should consult with a qualified financial advisor before making any investment decisions. Investing involves risks, including loss of principal.

Thanks for reading All In The Reflexes! Subscribe for free to receive new posts and support my work.