GDP growth data is a backward looking statistic; it tells you the story of where you’ve been, not where you’re going. Still, looking at where you’ve been can be helpful in charting the course of where you may be going. And in that sense, last week’s revision of the second quarter GDP growth data tells us we’ve been on a goldilocks path — housing and employment may look weak, but the rest of the economy is strong enough to more than make up for their weakness. If anything, the weakness is misleading, and if you are only focusing on the housing or labor stories, you’re missing the big picture.

That’s some people’s story, at least.

Thanks for reading All In The Reflexes! Subscribe for free to receive new posts and support my work.

Like in the stock market story, this data release is telling you all is well, powered by AI and the consumer. We’ve already looked at AI in the stock market story, so I don’t want to go into it too much, but the consumer and the stock market story are so intertwined that we’re going to have to hit it, at least a little bit.

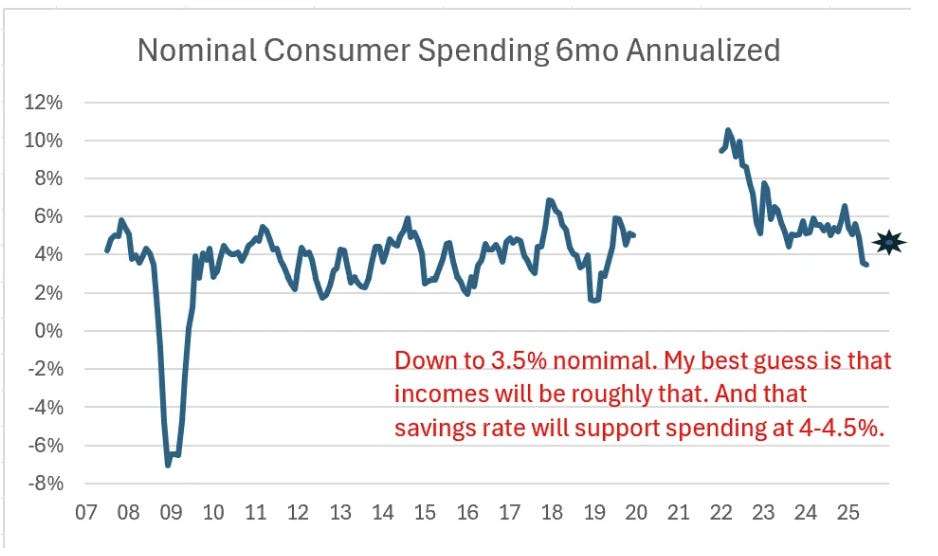

First, the direct consumer story. Consumption was revised up in the Q2 GDP data, so what originally looked like a sustained consumer slowdown now looks like an out-of-place blip.

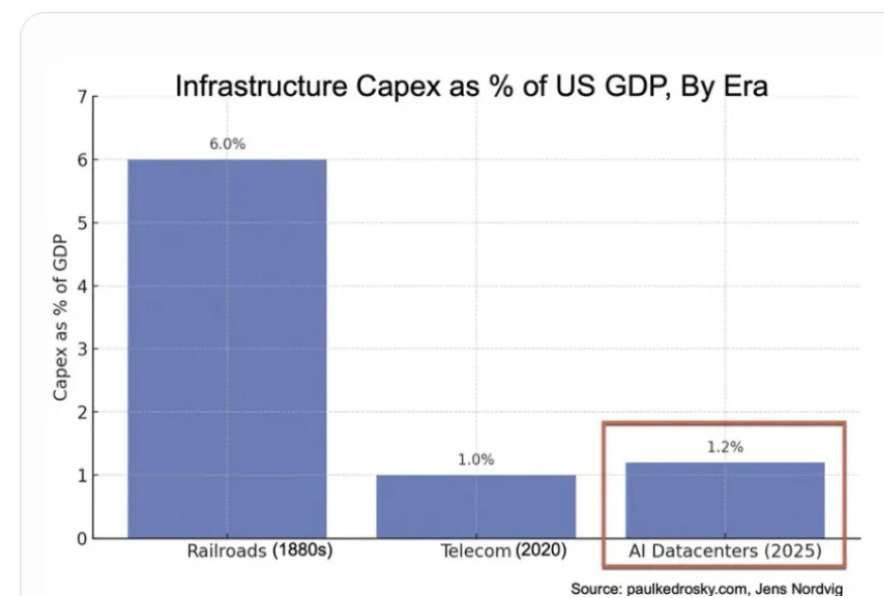

Second, the direct impact of AI. I’ve posted this chart in a couple of different articles already, but AI infrastructure investment is accounting for a massive amount of business fixed investment:

And—surprise, surprise—business fixed investment was also supportive in the Q2 GDP data.

Now, for the intertwining. The US consumer has been strong because they are wealthy from their stock investments (and housing, but we haven’t gotten to that story yet), and their stock investments are doing well because of AI.

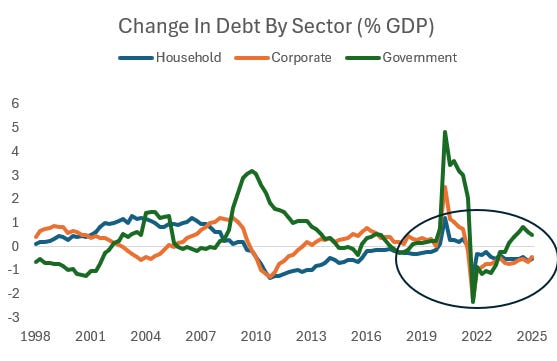

Consumer spending needs to be financed somehow. The most sustainable way to finance this spending is out of incomes — if incomes are rising, spending can rise at the same rate without any change in the savings rate (i.e., taking on additional debt). That is not what’s happening now.

And as my former colleague Bob Elliott points out, given the current pace of income growth, for spending to maintain its current pace, the savings rate would need to continue to fall.

And regardless, household borrowing is not the thing that’s driving this. The blue line is change in household debt, and outside of some Covid weirdness, they’ve been deleveraging since the Financial Crisis.

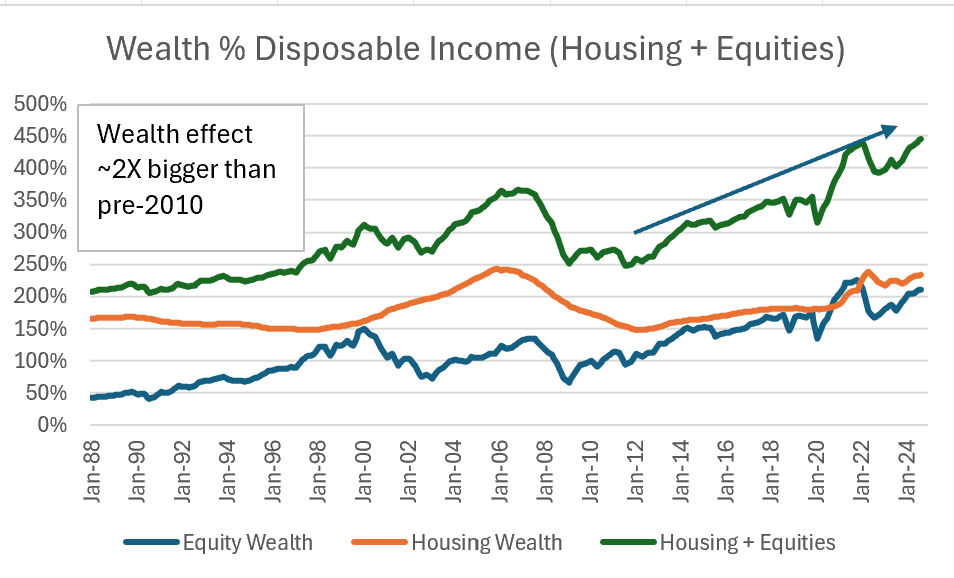

Jason Rotenberg, another one of my former colleagues, and the first person to tell me I should be writing this Substack, has been banging the drum for a while that it is the wealth effect that is driving the fall in the savings rate (and thus consumer spending).

Assets Levels and Changes Have Been the Driver

My version of household assets includes just equities and houses—market price-driven assets. However, any cut of assets or wealth would lead to the same conclusion.

The value of homes and equities owned by households is approaching twice what it was for much of recent decades.

These increases have been large and sustained since the global financial crisis. This long period of rising wealth could easily explain why many feel the need to save less. Over time, it becomes easier to extrapolate wealth gains.

A 15% rise or fall in equity prices today matters more than it ever did.

And putting this into growth impulse terms, he shows the massive change from Q1 to Q2.

So, to summarize, GDP is strong because AI investment and consumer spending is strong. Consumer spending is strong because consumers have lots of money from their house prices and stock prices going up. House prices, we’ll look at another day, and stock prices are going up because the stock market story is increasingly the AI story. So the stock market is mostly AI, business fixed investment is mostly AI, and the consumer is mostly AI via the stock market channel.

I’m sensing a theme.

Thanks for reading All In The Reflexes! Subscribe for free to receive new posts and support my work.