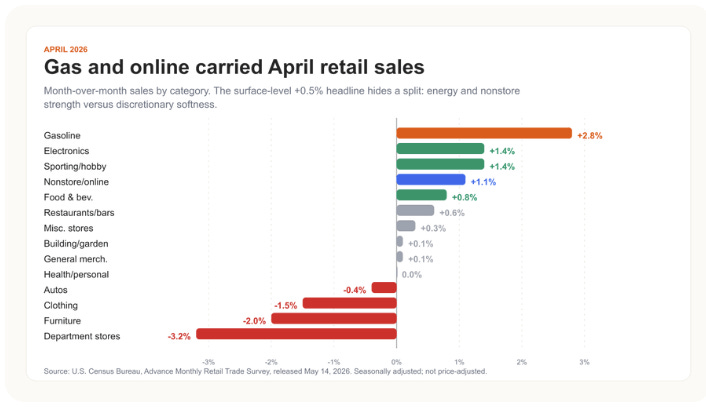

This month’s retail sales data shines a light onto how consumers are reacting to the energy shock and surge in gasoline prices. Unsurprisingly, gasoline spending surged and made up a large part of the strength. To offset that surge in necessary spend, consumers cut down meaningfully on most discretionary spending.

In real terms, this nominal spending came in below CPI leading to a negative real retail sales print at the same time that a greater proportion of that spend goes towards gasoline and away from discretionary spend

This is pretty much exactly the way I predicted it would play out.

Thanks for reading All In The Reflexes! Subscribe for free to receive new posts and support my work.

As I said in that post:

I think [the Fed] won’t ease because they just got burnt by Biden-era inflation even though this bout of potential inflation is clearly supply-driven. No amount of Fed easing can get more tankers through the Strait of Hormuz, so the net effect will be oil prices up, spending on non-oil things down, and therefore incomes down in the face of an already deteriorating labor market. That’s the recipe for falling demand, the one thing the Fed is set up to combat.

Falling demand is a deflationary impulse. In a supply shock, you get a sharp rise in the cost of the supply constrained good(s), which leads to a rise in measured inflation, but if those increased prices don’t lead to increased wages or spending power then overall spending will be down, which is deflationary.

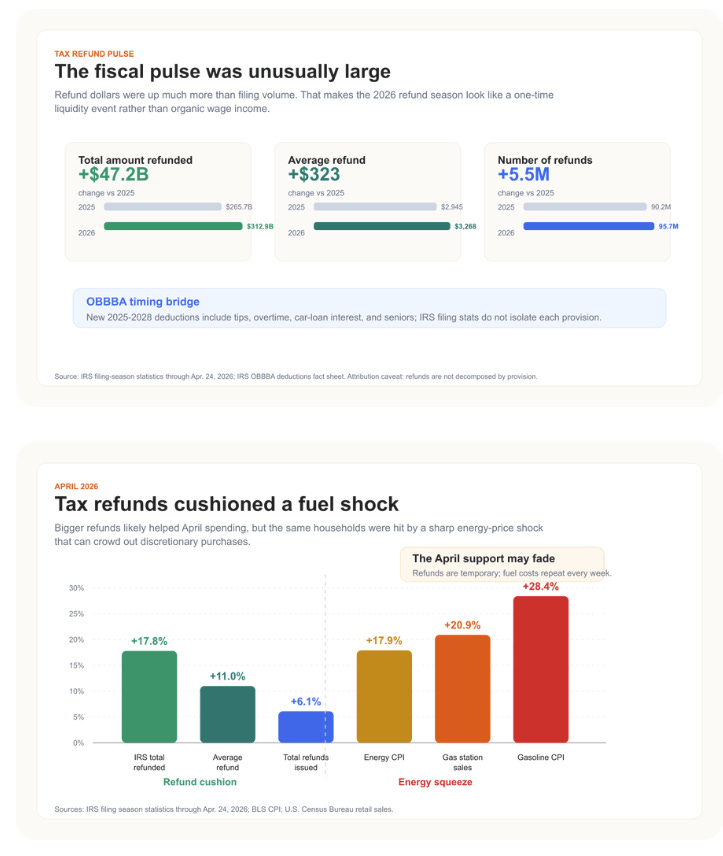

The key phrase there is “increased spending power”, because Jauvin points out there are other factors at play that are keeping spending power up.

And so, to answer the question of where the consumer resilience is coming from and how sustainable that resilience is comes into question to gauge how long the economy can weather this energy shock.

In some magical coincidence, the oil shock hit right as a OBBA related tax refund surge hit, providing a meaningful buffer to consumers to weather the storm:

These refunds hit at the perfect time to allow consumers to absorb this energy squeeze. Plus, a major equity rally rebound provided further confidence for households to dissave and draw down on their savings to make ends meet:

The combination of this dissaving and tax refund buffers are allowing the US economy to stay strong amidst this major energy shock. However, this dynamic cannot last forever and as consumption substitutes continue and households disave, eventually the chickens will have to come home to roost.

The most durable and reliable way to fund spending is through income (wages). Spending, while starting to crack a little, is still mostly holding up, but this is because of a confluence of factors — government transfers, dissaving, and stock market wealth that just keeps increasing — that won’t last forever.

That is, of course, unless AI truly is an infinite money hack and our technofeudal overlords deign to favor us with their beneficence.

News Scan

Drone Strikes UAE Nuclear Plant as War Threatens to Resume; Iran Submits Revised Peace Proposal

Source: Bloomberg / Reuters / ABC News Date/Time: Mon, 18 May 2026 Three drones hit the perimeter of the UAE’s Barakah nuclear power plant on Sunday — the first nuclear facility struck since the Iran war began — sparking a fire before two of three were intercepted. No radiological release occurred. The attack came as Trump posted social media warnings that “the clock is ticking” on Iran, and US and Iranian officials signaled readiness to resume open warfare if talks collapse. The contradicting signal: Iran simultaneously submitted a revised peace proposal to Washington through Pakistani diplomatic channels. The dual read — nuclear escalation and a back-channel negotiation — marks the ceasefire’s most volatile stretch, with Brent touching a two-week high above $109. The key question is whether the Pakistani channel produces a framework before US patience runs out. Bloomberg

Japan’s Takaichi Reverses on Extra Budget — JGB Yields Surge Toward 3%

Source: Bloomberg / Japan Times Date/Time: Mon, 18 May 2026 PM Sanae Takaichi called on Finance Minister Satsuki Katayama to compile an emergency supplementary budget to offset commodity shock costs — a full reversal after Katayama had explicitly ruled out additional spending just days ago. That “no extra budget” stance was the fiscal leg of the Japan triple tightening narrative (monetary + fiscal + currency simultaneously); its removal changes the Japan macro framework materially. Markets responded immediately: the 10-year JGB yield surged to 2.72–2.74%, the highest since the late 1990s, with strategists flagging potential for 3% within the year. The reversal complicates the BOJ’s June 15–16 decision in two directions — fiscal stimulus could embed inflation faster and push hikes forward, but the JGB selloff itself creates financial stability concerns the BOJ cannot ignore. Bloomberg

Italy Asks EU for Budget Flexibility to Absorb Energy Costs

Source: Bloomberg Date/Time: Mon, 18 May 2026 Italian PM Giorgia Meloni formally requested EU budget rule flexibility to allow deficit-financed absorption of rising household and business energy costs. The significance is the inflation channel: if the EU grants emergency flexibility — as it did during COVID — governments absorbing energy price increases via subsidies prevent the demand destruction that would otherwise make the supply shock self-correcting. Firms don’t cut output, workers keep jobs, wages stay elevated, and inflation embeds on the demand side rather than receding through market forces. This is the mechanism by which fiscal emergency measures shorten ECB hiking timelines; June 10 is live. Italy’s request is likely the first of several — watch for similar requests from Spain and France as the G7 Paris meeting accelerates pressure for a coordinated EU fiscal response. Together with Japan’s Takaichi reversal, this signals a G7-wide pattern: governments are absorbing the energy shock fiscally rather than allowing demand destruction, which embeds inflation and locks in a longer tightening cycle for central banks. Bloomberg

UK 30-Year Gilt Hits 1998 Highs as Hedge Funds Ramp Up Bearish Sterling Bets

Source: Bloomberg / CNBC Date/Time: Mon, 18 May 2026 The UK political risk trade sharpened materially this week: 30-year gilt yields hit 5.86% (highest since 1998), the 10-year reached 5.15–5.2% (highest since July 2008), and hedge funds explicitly ramped up bearish sterling options in response to Burnham’s campaign. Burnham attempted to give investors a mixed reassurance signal, but markets weren’t buying it — sterling has fallen five consecutive sessions. Polymarket puts Burnham at 42% to be the next PM vs. 27% for Starmer surviving. The specific risk is the Truss feedback loop: energy-driven inflation already elevated + Burnham’s association with heavier borrowing + gilt market already at multi-decade stress = each fiscal signal amplified. The 30yr move to 1998 highs is the clearest single-maturity signal that the market is pricing in structural deterioration of UK debt sustainability, not just political noise. Bloomberg

Global Bond Rout Grips G7 Finance Ministers Convening in Paris

Source: Bloomberg / Reuters Date/Time: Mon, 18 May 2026 G7 finance ministers gathered in Paris on May 18–19 with global bond yields at multi-decade highs as the dominant agenda item: Japan 10yr at 2.74% (30-year high), UK 30yr at 5.86% (highest since 1998), US 30yr at 5.12%, German 10yr at 3.18%. ECB President Lagarde voiced concern over the selloff during the meeting. JPMorgan’s fixed income team argued the Iran conflict has permanently “raised the floor” for yields by structurally embedding higher inflation expectations. The common thread is simple: oil-driven inflation is threatening to force central banks to hold or hike longer, compressing growth and fiscal positions simultaneously. This is the first multilateral attempt to coordinate a response to a bond repricing of generational scope — outcomes from Paris will determine whether the G7 moves toward coordinated communication or leaves each central bank to manage the repricing independently. Bloomberg

IEA Chief Warns Commercial Oil Inventories Are Falling “Very Fast”

Source: Bloomberg Date/Time: Mon, 18 May 2026 IEA Executive Director Fatih Birol delivered an unscheduled verbal warning that commercial oil inventories are depleting at an “accelerated pace” — a direct escalation from the agency’s formal May OMR (which reported a 250mb draw in March–April and a 146mb OECD draw in April alone). Birol rarely makes standalone verbal interventions outside formal reports; when he does, it signals a market development serious enough to require immediate public signaling. With summer demand peak approaching and OECD stocks down 4mb/d per month, the IEA is effectively putting governments on notice that strategic reserve releases or demand destruction are now the only near-term buffers before physical scarcity episodes. Bloomberg

US Allows Russia Oil Sanctions Waiver to Lapse — India Faces Supply Crunch

Source: KELO-AM / The Print / Bloomberg Date/Time: Sat, 16 May 2026 The US Treasury allowed to expire on May 16 a sanctions waiver that had permitted India and other countries to buy Russian seaborne crude without triggering secondary sanctions penalties. India had been importing 2.3mb/d of Russian crude at record levels — discounted Urals barrels used to compensate for the near-closure of Hormuz. With the waiver gone, Indian refiners face secondary sanctions risk if they continue sourcing Russian oil, forcing them to compete for alternative supply in an already structurally short market. Sanctions experts expect either a short-term extension or targeted exemptions to follow, but uncertainty itself is supply-tightening: India cannot contract forward without clarity, creating near-term scarcity while the diplomacy resolves. If no extension arrives, this adds roughly 2mb/d of displaced demand into an inventory-depleting market. KELO-AM

23 Tankers Cluster at Iran’s Kharg Island — Largest Buildup Since Blockade Began

Source: Bloomberg Date/Time: Mon, 18 May 2026 Shipping data shows 23 tankers congregating around Kharg Island, Iran’s principal oil export hub — the largest cluster since the US-led blockade began. The buildup carries two interpretations: Iran may be positioning for a mass export attempt (testing US enforcement capacity or responding to peace signals from the Pakistani channel), or vessels are consolidating ahead of anticipated escalation. Either reading is market-relevant — a successful Kharg breakout would be a supply-side event of immediate magnitude in a market drawing down inventories at 4mb/d pace. The timing is deliberate: the tanker cluster coincides with the revised Iranian peace proposal and the drone attack on Barakah, suggesting Iran is running simultaneous pressure and negotiation tracks, keeping the market guessing on its intentions. Bloomberg

China April Data Misses Broadly — Investment Contracts, Retail Sales Weakest Since 2022

Source: Bloomberg / CNBC Date/Time: Mon, 18 May 2026 China’s April economic data delivered a broad miss: fixed-asset investment contracted 1.6% YTD (reversing 1.7% growth in Q1), retail sales growth fell to its weakest since 2022, and the NBS flagged “grim and complicated” international conditions while calling for “more proactive fiscal measures.” This follows the April credit collapse (reported May 14: -10bn yuan vs. +300bn forecast) and confirms a structural demand problem that post-summit trade optimism cannot paper over. The NBS acknowledgment of a “prominent domestic supply-demand imbalance” opens the door to a larger stimulus response, but the Politburo’s absence of new concrete measures signals a wait-and-see posture on scale. The deflation escape question — whether Beijing will deploy sufficient fiscal force — remains open; this data makes it harder to sustain optimism that passive policy is sufficient. Bloomberg

EU Plans Mandatory Non-Chinese Component Sourcing for Chemicals and Industrial Machinery

Source: Reuters / FT Date/Time: Mon, 18 May 2026 The European Union is drafting regulations to require European companies in chemicals and industrial machinery sectors to source critical components from at least three different suppliers, with concentration caps limiting reliance on any single country — explicitly targeting Chinese supply dominance. The regulation extends existing “Made in Europe” procurement frameworks into mandatory supply-chain diversification rules. The macro implication is inflationary: forced de-sourcing from Chinese suppliers (typically the lowest-cost option) raises input costs in sectors that feed heavily into industrial output and capital goods, adding a persistent supply-side inflation layer on top of the energy shock. In aggregate, EU forced de-coupling + US tariffs + supply chain reshoring is compressing global supply-side flexibility at the precise moment that demand-side pressure from energy costs is already elevated. MarketScreener / FT

Disclaimer: The information provided on this blog is for informational purposes only and should not be considered investment, financial, or other professional advice. Nothing on this site constitutes a recommendation or solicitation to buy or sell any securities. You should consult with a qualified financial advisor before making any investment decisions. Investing involves risks, including loss of principal.

Thanks for reading All In The Reflexes! Subscribe for free to receive new posts and support my work.

Andrew, your farmer observation is the one that landed hardest for me — I'm in Kansas. When the heartland math stops working, it's not a leading indicator anymore. It's already happened.

Your 2007 comparison is apt too. What was hiding then was a consumer credit structure holding up a housing market that had already broken. What's hiding now is $1.1 trillion in credit card debt at 22% APR, with delinquencies at their highest since 2011, carrying grocery and gas purchases while the tax refund buffer Felix describes fades.

The dissaving isn't a confidence indicator. It's a desperation indicator wearing confidence's clothes.

Andrew, your farmer observation is the one that landed hardest for me — I'm in Kansas. When the heartland math stops working, it's not a leading indicator anymore. It's already happened.

Your 2007 comparison is apt too. What was hiding then was a consumer credit structure holding up a housing market that had already broken. What's hiding now is $1.1 trillion in credit card debt at 22% APR, with delinquencies at their highest since 2011, carrying grocery and gas purchases while the tax refund buffer Felix describes fades.

The dissaving isn't a confidence indicator. It's a desperation indicator wearing confidence's clothes.

Someone is paying attention. I wrote about the structural mechanism underneath this: https://lakesidegrammy.substack.com/p/killing-the-goose-that-laid-the-golden?r=4psz66