I have been consistently saying that if you want to understand where Federal Reserve policy is going, you should watch what Christopher Waller thinks.

So when Waller gives a speech, as he did at the tail end of last week, it’s worth listening.

There wasn’t really a ton of new information in the speech. He mostly reiterated his position that the Fed needs to get ahead of labor market weakening, due to the self-reinforcing nature of labor market weakening. This has all been said before, and I’ve even written about it.

Even so, there are a few interesting things to pull out of his speech. First, on where he thinks interest rates are going:

I believe the data on economic activity, the labor market, and inflation support moving policy toward a neutral setting. Based on the median of FOMC participants' estimates of the longer-run value of the federal funds rate, neutral is 125 to 150 basis points lower than the current setting. While I believe we should have cut in July, I am still hopeful that easing monetary policy at our next meeting can keep the labor market from deteriorating while returning inflation to the FOMC's goal of 2 percent. So, let's get on with it.

Second, on whether the prospect of tariff-driven inflation should keep the Fed cautious:

I believe that monetary policy should look through the tariff effects on inflation. With underlying inflation close to 2 percent, market-based measures of longer-term inflation expectations firmly anchored, and the chances of an undesirable weakening in the labor market increased, proper risk management means the FOMC should be cutting the policy rate now. I felt this way in July, and all the evidence since then has led me to feel more strongly about it today. Based on what I know today, I would support a 25 basis point cut at the Committee's meeting on September 16 and 17. While there are signs of a weakening labor market, I worry that conditions could deteriorate further and quite rapidly, and I think it is important that the FOMC not wait until such a deterioration is under way and risk falling behind the curve in setting appropriate monetary policy.

And third, on the speed at which cuts should take place:

While I judge that the FOMC should have begun this process in July, based on the data in hand, I don't believe that a cut of larger than 25 basis points is needed in September. That view, of course, could change if the employment report for August, due out a week from tomorrow, points to a substantially weakening economy and inflation remains well contained.

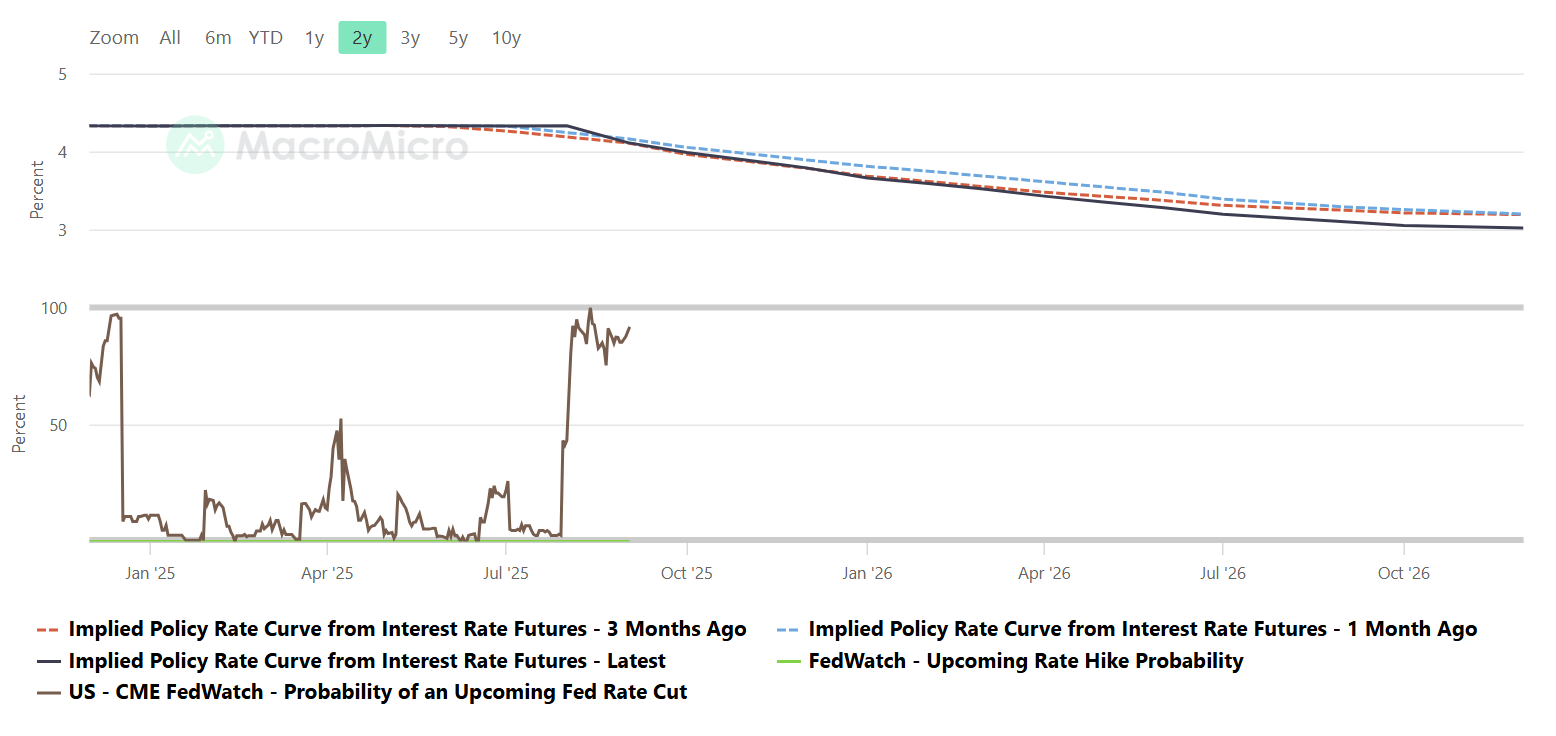

What I take away from all of that is that the base case for interest rates is 150 bps of cutting. This magnitude of cuts is what’s priced into interest rate markets, so the question really becomes one of how fast do we get there.

The gradual pace of cutting that’s priced in now seems in line with the overall message coming out of the Fed, but there are a few things to consider. The first is the symmetry (or lack thereof) of what could change the pace. It seems to me that Waller’s focus on inflation expectations remaining anchored and a belief that tariffs should be looked through, coupled with his worry about self-fulfilling downward momentum in the labor market, means that the path of least resistance is increasingly becoming faster cuts. This is on top of some political/institutional reasons to think that the Fed is leaning more towards cuts than remaining on hold or hikes.

It’s going to take a combination of inflation and employment surprising pretty big to the upside to slow the rate cut momentum, while all it will take for that momentum to become even stronger is another weak employment report on Friday.

Disclaimer: The information provided on this blog is for informational purposes only and should not be considered investment, financial, or other professional advice. Nothing on this site constitutes a recommendation or solicitation to buy or sell any securities. You should consult with a qualified financial advisor before making any investment decisions. Investing involves risks, including loss of principal.